Introduction:

Network realignment was a very hot topic at IDC Directions 2015 last Wednesday in San Jose, CA. We review selected presentations that cover the types of new mobility and cloud network transformations that will reside on the 3rd platform (cloud, mobile, social business, big data/analytics).

The major wide area network (WAN) transformation needed is one that moves from remote/central site private line/virtual private line connectivity to all sites having a reliable, available, and high performance connection to one or more Cloud Service Providers (CSPs). New strategies and partnerships are forming to address these challenges for wireless and wire-line carriers/MSOs as well as for newer players providing cloud connect solutions such as cloud exchanges.

Presentation Summaries & Take-Aways:

(1) During an early bird session on the big SMB Technology Reset, IDC’s Ray Boggs noted that on average, SMB outperformers (those citing net revenue gains in past year) were 61% more likely than the average SMB to prefer cloud delivery over on premise when deploying new IT solutions. Laggards (those citing net decreases in revenue over the past year) have almost the same response rate as the average. With a cloud access/delivery first model, SMBs need to revamp their WANs from the typical point to point private line/virtual private line or network model to one where all sites have high-speed/high availability access to cloud compute and storage resources.

Ray added that those same SMB outperformers are much more likely than the average SMB to prioritize mobile support (BoD, 3G/4G, WiFi) as a key 2015 spending priority. In particular, Small Business Outperformers are 58% more likely, Mid Market Outperformers are 60% more likely than the average SMB to have a solid mobile workforce strategy in place by 2015.

(2) In his morning keynote presentation on Tech Disruption and Data Center Transformation, IDC’s Rick Villars said that only 11% of WAN managers said they don’t need to change their networks to accommodate cloud services (likely because they weren’t planning to use them anytime soon). The remaining 89% of WAN managers are pursuing multiple options to realign their networks from the typical branch office-central site connectivity to more of a star topology where the majority of compute and storage services are delivered from one or more clouds. Some of the questions those managers were said to be concerned with were:

- Where’s Your Data? Is it stored locally, cached, or in the cloud?

- What’s In Your Service Catalog? For access by both internal line of business’ and external customers/partners.

- Is Your Network Congested? If so, how to alleviate it without too much over-provisioning?

- 50% of new IT hardware will be bought as a “converged bundle” in 2018. New software defined models (OpenStack, Hyper Convergence, Software Containers, etc) will influence IT hardware purchases.

- 58% of IT budget in 2016 will be for managed services.

(3) In a very intriguing presentation on Industry Clouds for line of business (LOB) to line of business communications, IDC’s Scott Lundstrom made these key points:

- Numerous examples exist in life sciences, biotech, financial services, retail, manufacturing, government, healthcare, and energy

- The number of Cloud Industry Platforms will expand to +500 by 2016, generating over a billion dollars in IT spending

- Industrial Data Lakes – Big Data on industry-specific platforms (e.g. GE, Merck, UHG)

- Industry platforms will disrupt 1/3 of the Top 20 Market Leaders in most industries by 2018

- Industry Cloud Participants include: existing enterprise suppliers, emerging cloud platform operators and networks, industry process and community specialists, services, software, and hardware vendors. Effectively, one Line of Business (LOB) to another LOB.

- New joint ventures will emerge

- Industry developer communities will gather and grow

- End users becoming suppliers – Global 2000

- LOB-2-LOB is the next B2B

Digital networks (LANs and WANs) are having a huge impact and disrupting business models:

- Innovation Accelerators drive change in every industry

- Connected products create new service opportunities

- Improving the process with sensors and automation

- Distribute intelligence and determine the next best action

(4) The spot on highlight of this year’s IDC Directions for me was Courtney Munroe’s presentation “The Future of Telecommunications Networking: Resurgence or Obsolescence?” With digital traffic and content continuing its exponential growth trajectory, and ARPUs flat or declining, both wireless and wireline telcos have an unsustainable business model. What steps they take to ensure their survivability depends on the market they’re addressing: wireless, residential broadband, enterprise wire-line, or cloud connect.

Consumer (wireless and residential broadband) market requirements for telcos:

- Manage the mobile data storm (Courtney didn’t say how – data caps?)

- Recognize that pure play connectivity/Internet access is dead. Instead, implement a multi-play strategy (Verizon, AT&T, and Comcast have certainly done that with their double and triple play bundles)

- Create an Over The Top (OTT) strategy – either alone or with partner companies. An example is Vodafone partnering with Dropbox to deliver cloud based storage for smart phones.

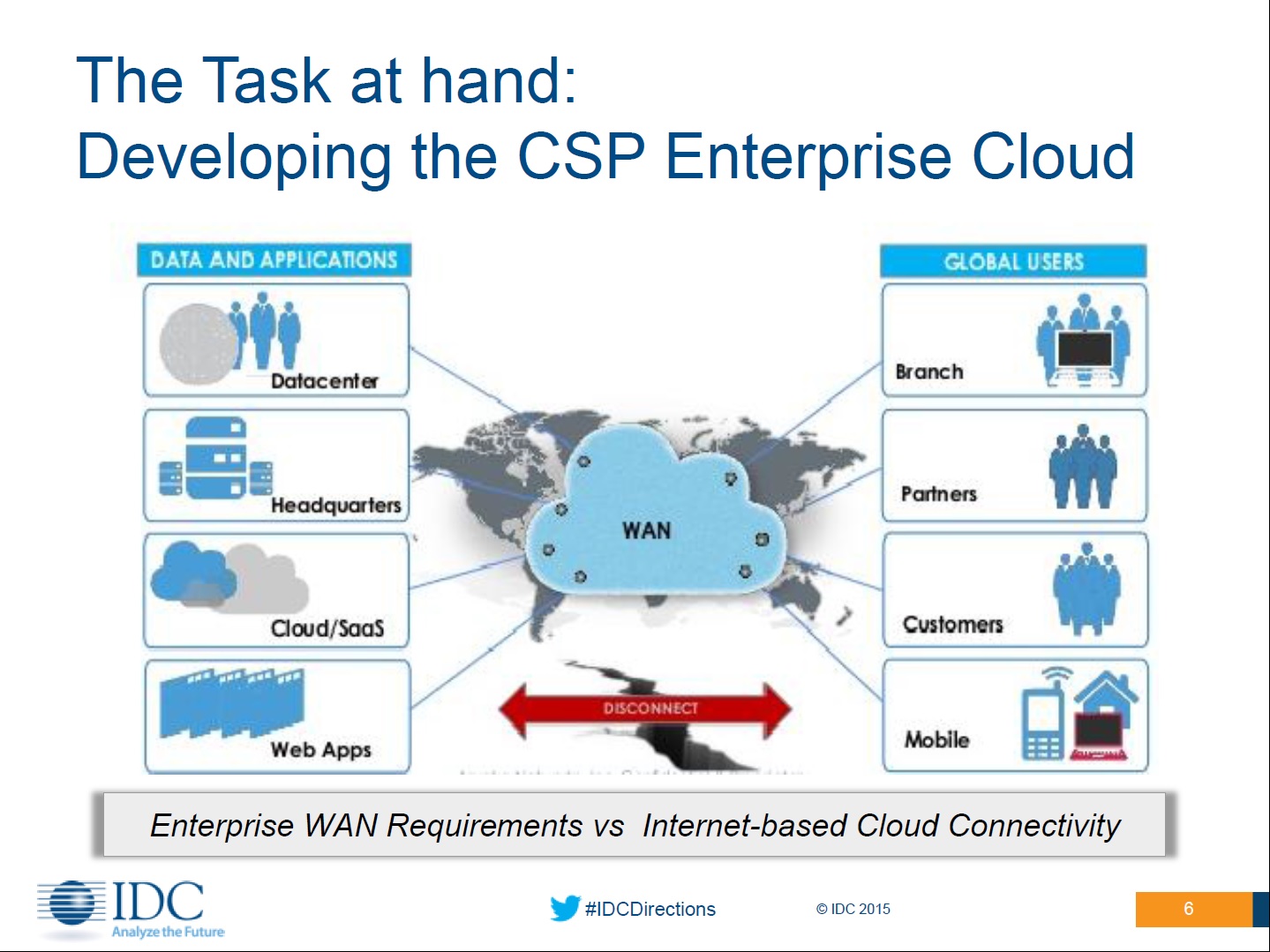

Enterprise market requirements for telcos: develop a Cloud Hub Enterprise WAN. This is best illustrated in the chart below titled: Enterprise WAN Requirements vs Internet-based Cloud Connectivity

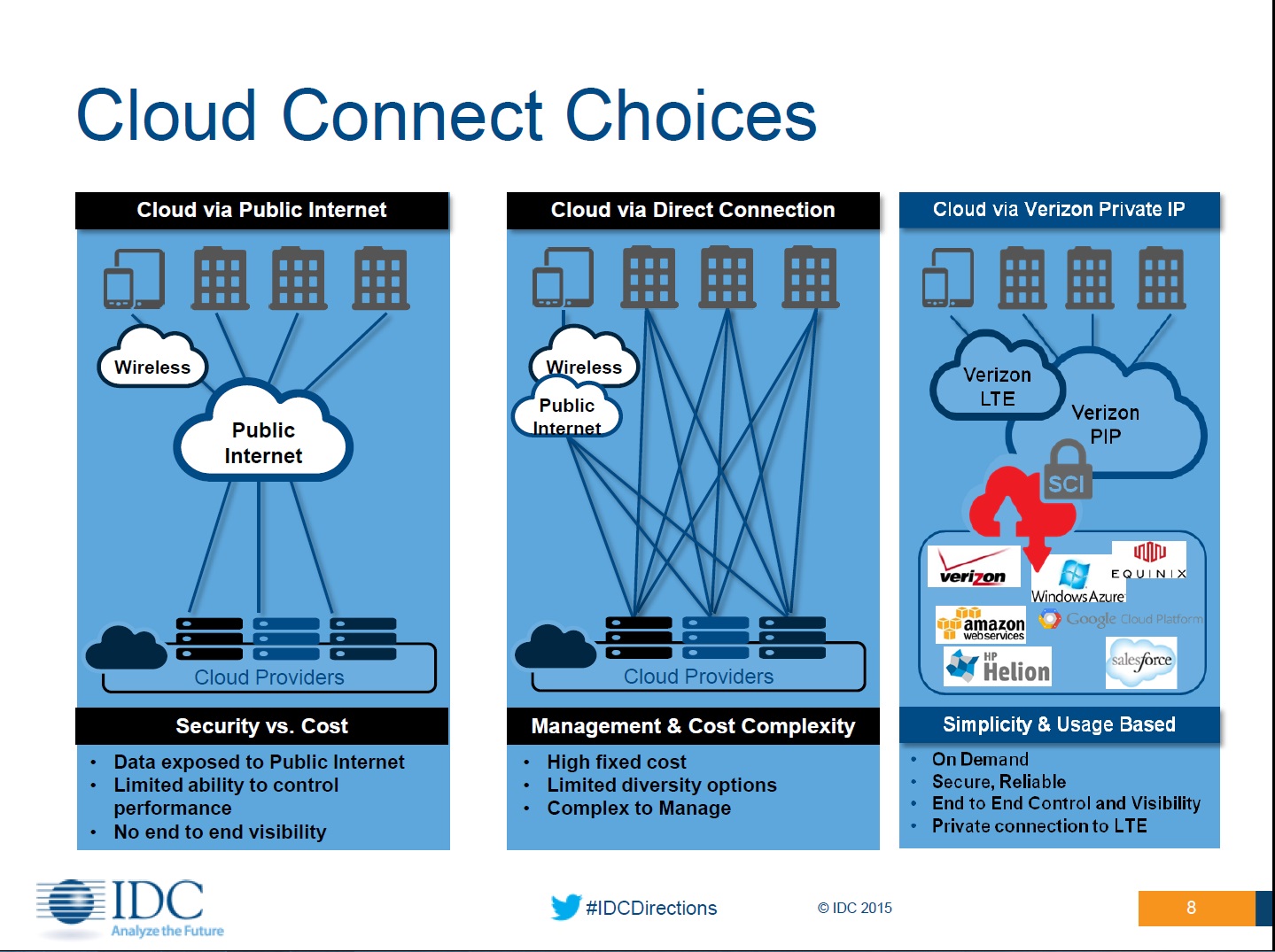

Instead of the plethora of connectivity choices for business customers to interconnect their geographically dispersed locations (private lines, Ethernet virtual private lines/LANs, IP-MPLS VPN, IP SEC VPN, etc) Courtney suggested that all physical sites should be cloud connected. The three choices today, depicted in the illustration below, are: public Internet, private line to CSP POP, and something equivalent to Verizon’s Private IP (one of several network operators that have a cloud network solution).

Among cloud networking solutions similar to Verizon’s Private IP: AT&T Netbond, Orange’s Business VPN Gallerie, NTT Com’s Enterprise Cloud (for NTT’s private cloud service only), Century Link/Savis IP-MPLS VPN, and specifications from the Metro Ethernet Forum on Carrier Ethernet for Cloud Service Delivery (although we don’t know of any network or cloud providers that have implemented it yet).

NFV was said to be “the new holy grail” for network operators as they’d then be able to virtualize and automate service creation and delivery. NFV examples include: vCPE, vFirewall, vVPN (???), vSet Top Boxes. Courtney said that telcos might be able to save 25% on operational costs and provide cloud based services. He identified AT&T, Telefonica, NTT/Virtela, and China Telecom as telcos that have announced NFV initiatives (Orange is also a leader in testing and deploying NFV in their SF research center). AT&T was quoted as saying that by 2020, 70% of their network would be virtualized.

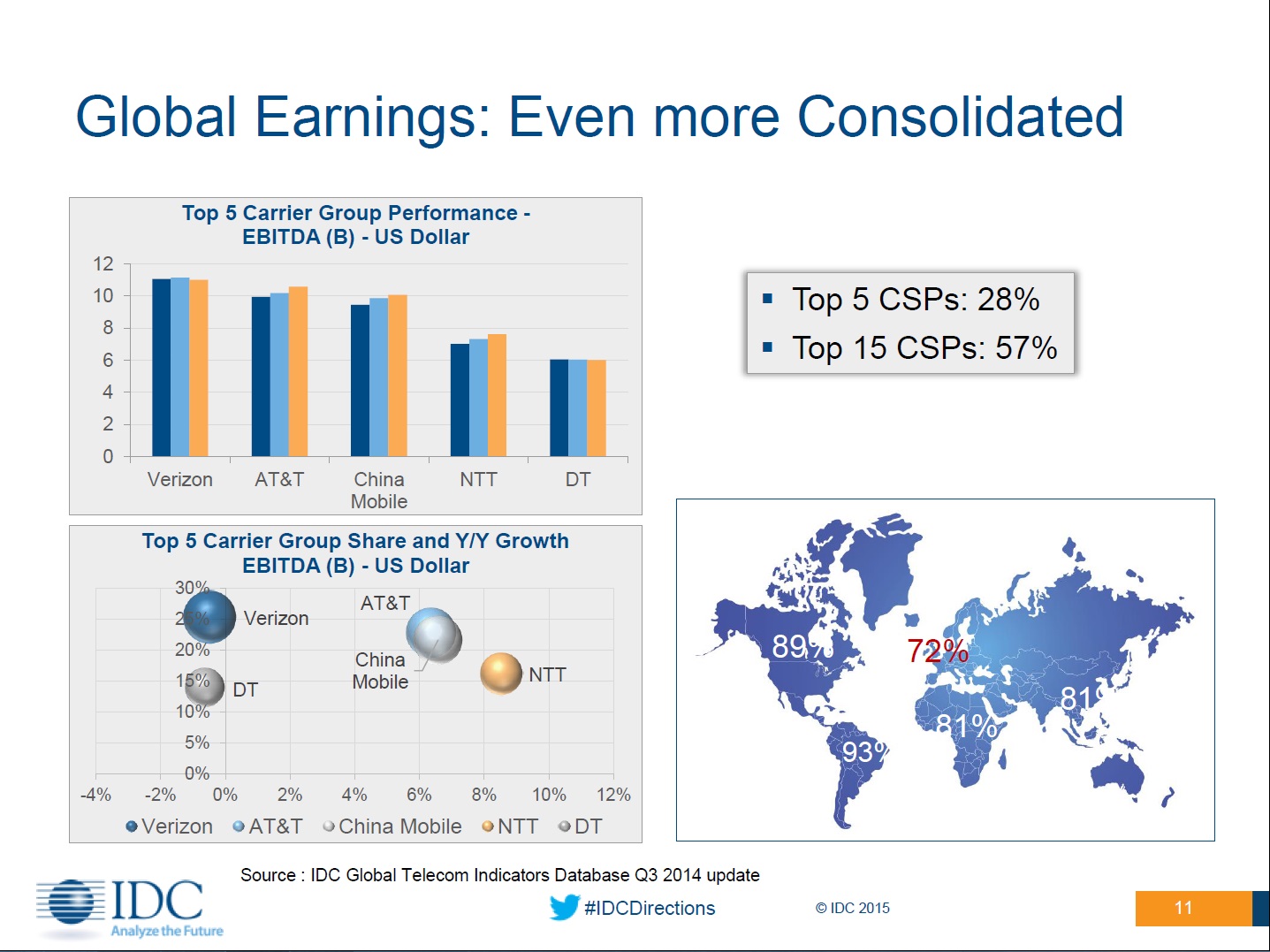

When it comes to global revenues and profits, the telco space is very concentrated with five major players: AT&T, NTT, Verizon, DT, and China Mobile as per the graphic below:

Consolidation is expected to continue in 2015. IDC say that there were ~100 telecom M&A deals in 2014 worth $262B.

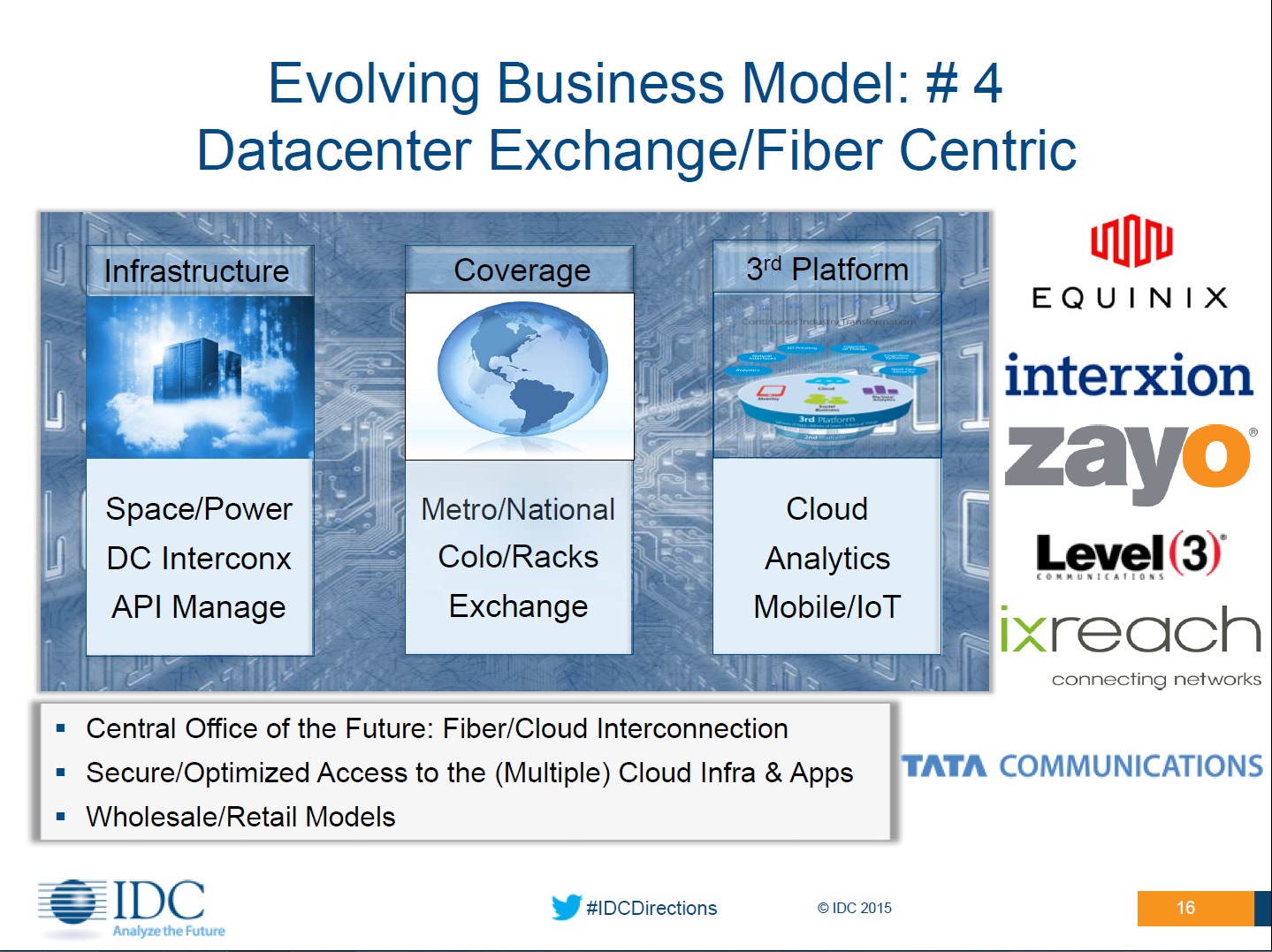

Mr. Munroe than presented six telco/MSO business models: mobile first operator, integrated multi-national super carrier, broadband/content first super carrier (mostly MSOs/cablecos), data center exchange/ fiber-cloud interconnection, cloud communications providers, and cloud VPNs. The Data Center Exchange/Cloud Connect/Cloud Exchange model is shown below:

For Data Center Exchanges/ Fiber Centric players, Courtney named several companies: Level 3, Tata Communications and Allied Fiber (see ViodiTV interview with Allied Fiber’s Hunter Newby). For Cloud Exchange, he cited: Equinix, Interxion, and Zayo.

Sidebar: Cloud Exchanges and Cloud Connect Solutions

For several years we’ve heard about cloud exchanges for interconnecting multiple cloud providers, but haven’t seen much deployment yet. Hosting and co-location providers realize that space and power are becoming a commodity service, so they are beginning to offer higher value cloud exchange or cloud connect services to provide direct connectivity for their customers to global carriers, ISPs, Internet exchanges, content and CDN players, storage vendors and enterprise and ecosystem partners.

“Cloud Connect” solutions allow co-location providers to offer enterprise customers high bandwidth, low-latency cloud connections that bypass the public Internet for superior throughput, reliability, security, and economics. Cloud Connect services combine the economics and service velocity of public clouds with the performance, reliability, and security of private connections.

Months ago, I asked a Comcast Business speaker how his company would provide cloud access to business customers he said “Cloud Exchanges” without any hesitation. We think this area deserves close watching in the months ahead.

Summing up with essential guidance for the telco/MSO space:

- Large Scale Super Carriers will strive for additional scale

- Cloud Exchanges will expand to Emerging Markets

- Cloud Platform Providers will become major Players

- SDN/NFV will create long-term investment opportunities

- CSPs need help developing Channels (vertical solutions, IoT developers, VARs/OEMs/Systems Integrators, and OTT players)

- Developers will become important CSP Partners (we think that will be especially true for OTT and IoT solutions)

It will be very interesting how all this plays out as the move to the 3rd platform accelerates in the years ahead.

References:

- IDC Directions 2015 Preview Videos

- IDC Directions 2015 Agenda

- IDC Directions 2014: 3rd Platform is Transforming and Disrupting IT; IoT Offers Tremendous Potential!

- 2013 IDC Directions-Part I: 3rd Platform, Cloud Spending & Apps, Global Economic Trends

- 2013 IDC Directions Part II- New Data Center Dynamics and Requirements http://viodi.com/2013/03/17/2013-idc-directions-part-ii-new-data-center-dynamics-and-requirements/

- 2013 IDC Directions Part III- Where Are We Headed with Software-Defined Networking (SDN)?

- Key Messages from IDC Directions 2012 for “The Intelligent Network” – Part 1

- Key Messages from IDC Directions 2012 for “The Network” – Part 2

Leave a Reply